Accounting for Excess Reportable Income (ERI) primarily involves specific UK tax reporting for investors in offshore reporting funds, rather than standard accounting entries within the fund itself. The ERI amount is a notional distribution used for tax purposes.

Investor Accounting and Tax Treatment

For a UK resident investor holding units in an offshore reporting fund outside of a tax-wrapper (like an ISA or SIPP), the accounting involves two key aspects: income tax reporting and capital gains tax (CGT) base cost adjustment.

1. Income Tax Reporting (Self Assessment)

The ERI is treated as a form of taxable income (either interest or dividend, depending on the fund's underlying assets) that the investor is deemed to have received, even though no cash was distributed.

- When to report: The ERI is accounted for in the tax year that the Fund Distribution Date falls into. This date is typically six months after the fund's reporting period end date.

- How to report: The investor reports the ERI on the "Foreign Pages" (SA106) of their Self Assessment tax return.

- If treated as interest, it goes under "Interest and other income from overseas savings".

- If treated as a dividend, it goes under "Dividends from foreign companies".

- Data source: Fund managers provide this information in an annual report, typically available on their website or in a consolidated tax certificate. The amount is calculated as the ERI rate per unit multiplied by the number of units held at the end of the reporting period.

2. Capital Gains Tax (CGT) Base Cost Adjustment

To prevent double taxation (once as income, and again as a capital gain upon disposal), the total ERI on which the investor has paid income tax is added to the original base cost (acquisition cost) of their investment.

- Impact on disposal: This increased base cost reduces the eventual capital gain (or increases the loss) when the investor sells their fund units.

- Calculation: Capital gain = Net proceeds – (Original base cost + Total ERI previously taxed).

Internal Accounting (Journal Entries)

From an investor's personal accounting perspective, the ERI would be recorded to reflect the increase in the investment's value and the corresponding tax liability. A simplified conceptual journal entry (not a formal accounting standard entry but useful for tracking) would be:

- Debit: Investment Asset (to increase the book cost/base cost)

- Credit: Income Tax Liability / Income (to recognise the taxable event)

This adjustment ensures the investment's carrying value is consistent with its tax base cost, which is crucial for accurate CGT calculations later.

How to enter ERI in Troika

Within Troika Wealth Management, there it a new investment transaction type – 'Excess Reportable Income'.

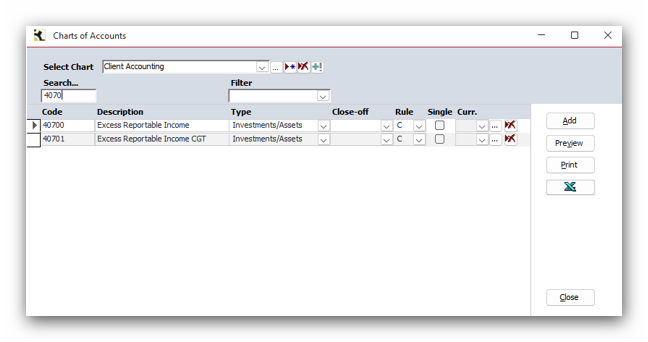

Firstly, within the Chart of Accounts menu option, add two new codes. Our suggestion would be as follows, but this will depend on your current nominal code structure:

Dr and Cr Balance sheet Code.

Remember to add these new codes to the relevant clients.

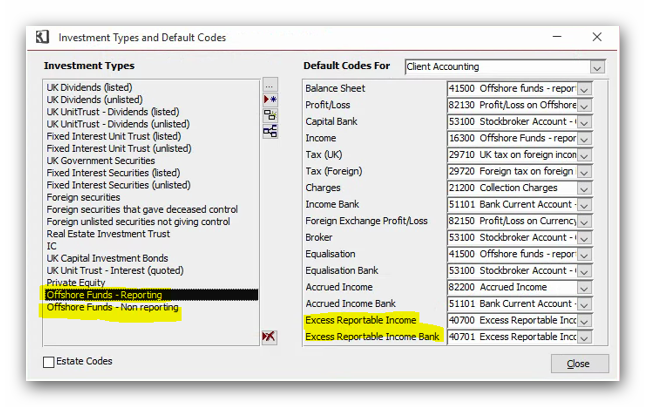

Once the codes have been added to the chart of accounts, they need to be added to the Investment Types and Default Codes, within Utilities, and the Database tab:

Once these have been added, you can assign the relevant Investment Type to the new investment you are setting in Wealth Management, Investment Details.

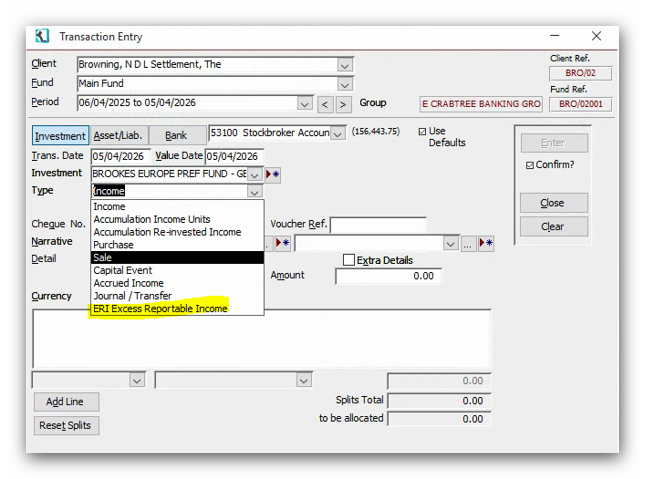

To post the journal, navigate to Transactions – Add and click on the 'Investment' tab. After entering the relevant dates and choosing the investment, you will now see the new journal type available within the transaction 'Type' drop-down list:

Click on that type and then enter the distribution amount. You will see the codes for that investment type appear.

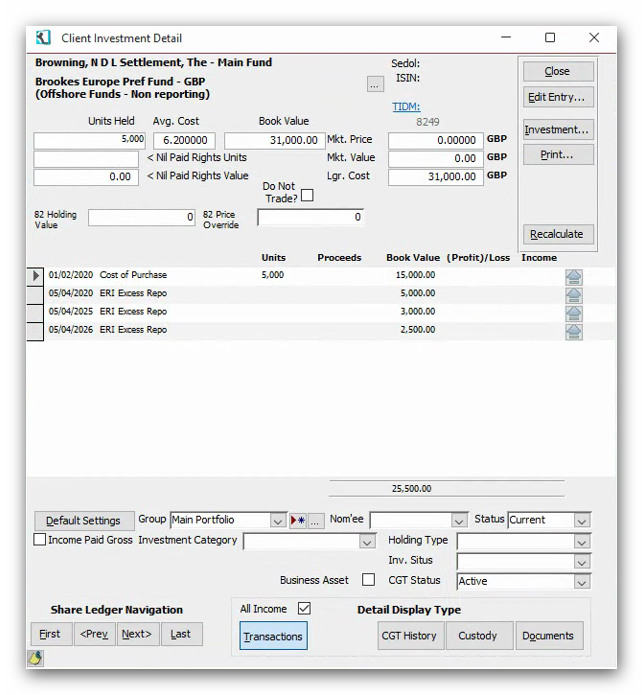

Once posted the journal will appear on the relevant investment ledger as:

This article is confirmed to be applicable from Troika release 2.09.026.

This article was last reviewed 06/2026.